| Latest Forum Topics / Biosensors |

|

|

Is Biosensors a good buy?

|

|||||

|

bengster68

Master |

29-Jan-2008 15:42

|

||||

|

x 0

x 0 Alert Admin |

I bought some more at 75 cts and 75.5cts today. I told im still in buying mode. To me, BIG is a $3 stock. Im not like some forumers that will tell you this stock is good after they bought and will chiong, then tell you this stock is hopeless after they have sold or shorted it. |

||||

| Useful To Me Not Useful To Me | |||||

|

ekekeg

Veteran |

29-Jan-2008 15:37

|

||||

|

x 0

x 0 Alert Admin |

This KNN market has dashed many BIG supporters' hope for a happy new year in 2008. Many retail investors are slaughtered left and right and I really think it will take a bit of time before the brokers get busy again. Unless Wall Street shows a couple of straight gains in the coming weeks. But if you have spare cash sitting in the fixed deposits, this is the best time of your life (maybe) to take them out and whatever amount you can into the market. All shares are going for lelong; some 75% to 85% off their highs and some even less than 5% above their lowest ever compared to last year. | ||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

Younglady

Member |

29-Jan-2008 15:23

|

||||

|

x 0

x 0 Alert Admin |

huh so beng star u buy part of it again??? it was lower than u buy at 0.8cents I find that now quite good price also, but duno will it be under control. hahhaa. So scared yeah |

||||

| Useful To Me Not Useful To Me | |||||

|

gbleng

Member |

29-Jan-2008 14:41

|

||||

|

x 1

x 0 Alert Admin |

Yes..one last thing he needs to do is to have a bath in flower water and consult a fengshui master... otherwise all the good things kena bashed up by the bad.. like this stock melt down... pure bad luck Ang pow money gone for the time being | ||||

| Useful To Me Not Useful To Me | |||||

|

bengster68

Master |

29-Jan-2008 13:02

|

||||

|

x 0

x 0 Alert Admin |

The ex-CEO has the biggest stake in this company. He is the best person to do the job of negotiating very large deals. These deals will have the most material impact to the share price and requires his full attention. See how the internal corporate direction is moving? LYC is not taking a "backseat" after CE approval. He is doing the most important job now that no one else is more qualified than LYC: to close BIG deals and bring up shareholders value. Leave the operations and responsibility like capturing more market share to the ang moh professional. Get the picture clearer now? | ||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

EastWind

Member |

29-Jan-2008 12:21

|

||||

|

x 0

x 0 Alert Admin |

It is very unfortunate that the first trading day post-CE occurred last monday when stock markets went into a tail spin. There are many who questioned the 'low' price of this stock right now. My response is - when a tsunami hits, nothing is spared.. The true value of this company is not going to be achieved overnight. Was anyone expecting BIG to immediately start selling millions of stents the day after CE? Of couse not! Its going to take time. This is where BIG's last annoucement about the top corporate changes is so important and significant. It is obvious that, like many of BIG's corporate moves, this one was planned in an orderly fashion some time ago, as indicated by the annoucment so quickly after CE was approved. Why is this good? For the founder and biggest shareholder to relinquish his CEO post means that there are no egos in this company. Instead, the company concentrates on getting the best person for the job. This means that Mr Lu is freed up to unlock shareholder value and Kleine will concentrate on what he does best - sales. I believe that Mr Lu will now concentrate on eventually getting a takeover done. But no predator will buy you at a hefty takeover premium. Conversely, BIG is unlikely to sell unless they get that hefty takeover premium. As an illustration, if BIG wants to sell out at $3, it means a hefty premium of around 300% over today's price. However, if its share price is at $2, the takeover premium shrinks dramatically and is certainly more palatable to a predator. So the new CEO has to dramatically increase sales. Once that happens, we should see the share price move up. It should not be too difficult as BIG is starting from a zero base. If you have observed this company, you will realise that they do things carefully and always with a grand vision in mind. Whether that grand vision ends up with BIG being a stand alone company or being taken over, we shall see but either way, I believe that the shareholder will eventually be rewarded. Not an inducement to buy/sell. Its your money and you decide. |

||||

| Useful To Me Not Useful To Me | |||||

|

bengster68

Master |

29-Jan-2008 11:42

|

||||

|

x 0

x 0 Alert Admin |

Yes of course Part 2 in progress. Look at what Raffles Education is doing. I think there is a possiblity BIG can corner the whole china market very soon because one of their main competitor in China is now under investigation for bribing the China ex-SFDA chief who was executed last year for corruption. Apparently, there was no clinical trial done and it was approved for sale in China back in 2003. If the authorities decide to ban the competitor's DES, JWMS will corner about 80% of china market easily. JWMS has CREATE clinical trial involving 2,000 patients (a strong potfolio) to back back its claims. | ||||

| Useful To Me Not Useful To Me | |||||

|

Impossible

Member |

29-Jan-2008 11:03

|

||||

|

x 0

x 0 Alert Admin |

Bengster, Is part II still in progress? Any timeframe? Thanks. |

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

ekekeg

Veteran |

29-Jan-2008 10:10

|

||||

|

x 0

x 0 Alert Admin |

I think the proper pricing of a share should be based on several factors and not just how much it is worth in terms of PE or earnings because these will change when other fundamentals are changed. Example of changes will be market sentiments, contracts arising, intrinsic goodwill and earned goodwill and a host of other properties. By instrinsic goodwill, I mean the amount of money already well spent on R&D giving the company an intangible but virtual benefit over companies where less R&D expenses are incurred. Earned goodwill will be things like CEs and other approvals for marketing approved by controlling authorities. Therefore I believe a number of analysts are quite near with their fair price for BIG shares around 1.20 to 1.50 cents per share. Naturally this price will surge if there are potential for takeovers by "predators". And idf BIG returns profitable soon, then I would say it will be worth more. Having said this, investors should also be cautious about some form of manipulations by BigBoys who trade against you. You cannot beat them because they are the giants and we are the immobilised davids.. If they are short, they will press the price further down, but if they are long then at least we can ride the wave to profit as the price climbs up. |

||||

| Useful To Me Not Useful To Me | |||||

|

bengster68

Master |

29-Jan-2008 10:09

|

||||

|

x 0

x 0 Alert Admin |

Biomatrix Freedom is not totally bioabsorbable. It leaves behind as a BMS. Biomatrix-Freedom and Biomatrix is very similar, except Biomatrix-Freedom do not use polymer. However, BIG has a totally biogredable DES made out of PLA and BiolimusA9 which is something very similar to ABT's ABSORB DES. I think BIG's totally bioabsorbable DES uses the spring coil strut design to prevent the stent from collapsing inwards since there is no metal backbone in the stent's structure. There is a company called Reva Medical (BSX is a main shareholder in this start up). Reva uses Paclitaxel drug and "clip and lock" strut design to prevent the biodegredable polymer from collapsing inwards. Bioabsorbable material's patent is not as powerful as technology/technique patent. "Any limus drug on biodegredable polymer" encompasses a very wide range. If you uses any kind of Limus family drug on any kind of biodegredable polymer (need not be PLA biodegredable polymer), you will be in breach. The net is very wide for this patent. Ignore shortists posting that BIG is a loss making company, my broker say BIG going to kena selldown to 50cts, etc. They are trying to instill fear to forumers so that they can cover back their short positions cheap. Shortists that have shorted always need to buy back the shares. Do not sell your shares cheap. I assure you that you will not regret holding on to BIG shares. Im still in accumulation mode and may end up buying your shares. In fact, i bought some more yesterday. |

||||

| Useful To Me Not Useful To Me | |||||

|

PensionAlterEgo

Member |

29-Jan-2008 09:07

|

||||

|

x 0

x 0 Alert Admin |

Another question to add for bengster. Do you know who owns the patent for bioabsorbable DES? Any of the big players such as JnJ or Abbott? I did a google search and found a patent for a more general bioabsorbable material for use in cardiovascular applications, among other uses.. and it's assignee is Tepha Inc. a medical device company...with possible link to Novartis. I think the main concern is whether Biosensors could be sued for such a DES if they do not own the patent. |

||||

| Useful To Me Not Useful To Me | |||||

|

novena_33

Veteran |

29-Jan-2008 08:26

|

||||

|

x 0

x 0 Alert Admin |

sound like they still have a good story to tell there.....

|

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

gbleng

Member |

29-Jan-2008 07:13

|

||||

|

x 0

x 0 Alert Admin |

Hi bengster, how do compare this with BIG's biomatrix Freedom.... they are both the same type right? Which is more advanced in its development? | ||||

| Useful To Me Not Useful To Me | |||||

|

bengster68

Master |

29-Jan-2008 01:00

|

||||

|

x 0

x 0 Alert Admin |

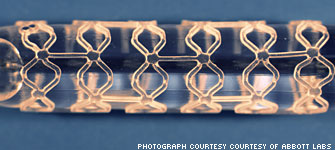

It sounds like science fiction: A stent made of bioabsorbable plastic simply dissolves back into the bloodstream within a year or two after its work opening an artery is done--similar to the way sutures or bone screws are ultimately absorbed. Stent designers have spent decades pursuing this goal, with little success. But drug and medical-devices company Abbott Laboratories (NYSE:ABT) --the leader in old-style, bare-metal stents, with $24 billion in revenues--is finally showing progress. Abbott's new stent, called Absorb, is made of polylactic acid and coated with a drug called Everolimus; the water in the artery wall eventually breaks down the polylactic acid into lactic acid, a naturally produced substance. That lactic acid is then absorbed into the body as carbon dioxide and water, leaving nothing behind. Absorb's human trials in 30 patients showed positive results at the nine-month mark, with a low rate of major cardiovascular events and no stent thrombosis, a rare but often fatal clotting within the stent itself years after insertion. This makes the goal seem increasingly possible. "If I could provide a fully bioabsorbable, drug-coated stent that works as well as a metallic one, it's a no-brainer," says John M. Capek, Abbott's executive VP for medical products, who announced the initial results last fall. "Why wouldn't you pick the one that returns the vessel to a more natural state? If you define the question that way, it could be the only stent we're using in the future." Abbott is still tweaking its design, but hopes to receive FDA approval for release in the United States in 2012; it could begin marketing in Europe even earlier. This development comes at a welcome time for an industry that has hit a speed bump. Medical concerns about late-stent thrombosis reversed the medical device's sales momentum. Stent revenues in 2007 are expected to dip to $5.2 billion, from a high of $6.3 billion in 2006. While there are some indications the concerns were overstated, all of the major manufacturers-- Absorb's story began five years ago with Dr. Richard Stack, a retired interventional cardiologist at Duke University and founder of SyneCor, a medical-devices think tank. SyneCor developed the basic technology in 2002 and sold it to Guidant in 2003 (when Capek got involved). Abbott acquired Guidant's vascular business in 2006. The researchers didn't want to lose themselves and their work in the bureaucracy of a big organization like Abbott, so their lab remained in Santa Clara, California, far away from Abbott's Chicago-area headquarters. To speed up research, they reorganized the assembly-line process and connected the designers' computers directly to lasers to cut the lag time between design and manufacturing. Abbott ultimately slashed the time it took to make a new design from months to weeks, then to just one day; to date, the company has designed and manufactured some 300 different iterations of Absorb. By reducing the time it took to design, "we didn't need the first one to be right," Capek says. "We can have one or two failures and still beat our schedule." He hopes to roll out this production process to other areas within Abbott. By playing around with the design, they solved the conundrum they'd had with performance. Could a polymer stent that's meant to be absorbed into the body within a year or two be as good at holding an artery open as a traditional metal one? The new iterative process, which allowed the stent researchers to try many options, was critical because polymers have a lot more variables than metals--the thickness of the stent, the processing of the polymer, and so forth. Polymers are not as strong as metals, and when you try to make them stronger, they become brittle. Researchers discovered that by making the polymer stents slightly thicker than Abbott's traditional ones, they gained durability without triggering additional adverse reactions. The challenge now is to get the absorption time right: If the stent dissolves too quickly, the artery may not remain open long enough and the patient would then be at risk for a heart attack. But if it goes too slowly, then there's less advantage over a traditional stent. And the faster you want the stent to dissipate, the harder it is to make it durable. Abbott's current lab studies show absorption rates of two-and-a-half years, says Richard Rapoza, Abbott's divisional VP in charge of Absorb. Researchers hope to cut that to one and a half. "A shorter absorption time may be achievable and better for marketing," he says, "but we don't want to push it down too far." Finally, and perhaps most intriguing, researchers hope that by opening the artery and returning it to a natural state, an absorbable stent could help the body to heal itself. This remains the biggest open question for Absorb, one that will be resolved through additional human trials. "If you hold the vessel [with the stent] and enable it to grow as it receives signals from the body, then we can reestablish the healing curve and get rid of the problems that we see with metallic stents," explains Rapoza. "That's the really big promise of the technology."

This is Not a Caterpillar Molting Rather, it's an actual bioabsorbable coronary stent system to be used in a human patient in Abbott's trials for Absorb. *** How to value BIG is very individual. My value for BIG's patent of "any limus drug on biodegredable polymer is US$500m. Most investors value this patent as zero. ABT's ABSORB DES is clearly in breach of BIG's patent. BIG can demand a lump sum payment of US$150m plus royalty of sales at 20% for patent breach. Otherwise, BIG can institute a worldwide injunction against ABSORB DES to stop their sales after regulatory approvals. JWMS's EXCEL DES was also in breach of BIG's patent. If not, why would JW's previous shareholders be willing to sell off this company? Legally, BIG can "destroy" the whole JWMS company for patent breach if the owners refuse to sell their shares. |

||||

| Useful To Me Not Useful To Me | |||||

|

investor

Senior |

28-Jan-2008 20:29

|

||||

|

x 0

x 0 Alert Admin |

Is is an interesting question - What exactly is the fair value of Biosensors ? Somebody has mentioned 0.55 cents - what is the basis ? Traditional yardstick of measurement is by NBV (Obviously with this method, BIG is definitely not worth 10 cents, let alone 0.55 cents). ANother method, is by the discounted cash flow method, whereby projected cash flow is discounted back to present value. Other methods, might be based on prospective PE ratio, inline with its peers in the same industry. Most analyst have a target value of 1.23 - 1.40 for BIG, base on DCf or PE ratio, etc. Other layman's approach might be base on what others are buying BIG at - eg, Shandong Weigao is willing to sell its highly profitable JW Medical in exchange for BIG shares at 1.08, and it has an option to buy more shares using cash, probably also at 1.08 - Do they know something that we don't know ? What about the venture funds - buying convertible bonds in BIG that can only be converted into shares at >1.00 ? SO, what is the value of Biosensors ? - A good question - Any answers ? - Based on the factors that we do know ? |

||||

| Useful To Me Not Useful To Me | |||||

|

bengster68

Master |

28-Jan-2008 18:39

|

||||

|

x 0

x 0 Alert Admin |

Takeover of small pharmaceutical/biomed companies at 100% premium from last traded price is not uncommon in USA. Takeover of Conor was around 30% from last traded price but a couple of weeks before takeover Conor's share price has been climbing up steadily by 20%. Maybe news leaked out from Conor??? I feel BIG's takeover premium when it happens will probably be 100%. This high premium is not because the buyer overpaid for BIG but BIG is too unappreciated by investors here. | ||||

| Useful To Me Not Useful To Me | |||||

|

OkieDokie

Member |

28-Jan-2008 18:24

|

||||

|

x 0

x 0 Alert Admin |

Take-over by JnJ ??? Certainly won't happen around this time, even if both buyer/seller has already agreed on the deal,say at $2 transacted price ! How can JnJ explains the excessive premium to their public shareholders ??? First, buyer/seller must stage the price recovery of BIG closer to transacted price, say about plus minus 10 to 20 percent. So in my opinion, there is no takeover in sight meanwhile. Only when I see the price moves up (lots to do from today price) will I think the takeover is in he process. Dun think key shareholders will sell even if any of BBs offer 100% premium over today price. I won't for sure, not unless they I am force to when the prospective buyer has already achieved 90% outstanding shares acceptance. LYC, CKL and RMK better have something up their sleeves ! Better pull out a white fat rabbit and not a Peh-Ban (mahjong blank card) or Ang Tiong out from the hat ! Really shagged !!! But still hopeful ! |

||||

| Useful To Me Not Useful To Me | |||||

|

dcang84

Veteran |

28-Jan-2008 17:56

|

||||

|

x 0

x 0 Alert Admin |

< How can you say J&J not stupid when they used $1.4b to buy a lousy company. My guess is they will buy Biosensors eventually > Dream om......  |

||||

| Useful To Me Not Useful To Me | |||||

|

superbad2

Member |

28-Jan-2008 17:21

|

||||

|

x 0

x 0 Alert Admin |

Anything below 70 can buy and close eyes. If it ever reaches there. however, this stock has shown not to move much when dead cat bounce. So dun try to get short term gains. |

||||

| Useful To Me Not Useful To Me | |||||

|

limhpp

Veteran |

28-Jan-2008 17:02

|

||||

|

x 0

x 0 Alert Admin |

Thanks! Noted

|

||||

| Useful To Me Not Useful To Me | |||||

x 0

x 0  x 0

x 0