Federal Reserve Bank of St. Louis President James Bullard, a voter on policy this year who has backed record stimulus, said the

Fed may make a small cut to bond purchases in October after its narrow decision this week not to reduce accommodation.

?

That was a borderline decision? after ?weaker data came in,? Bullard said yesterday on Bloomberg Television?s ?Bloomberg Surveillance? with

Tom Keene and Sara Eisen. ?The committee came down on the side of, ?Let?s wait.??

Bullard called October a ?live meeting,? because ?it?s possible you could get some data that change the complexion of the outlook and could make the committee be comfortable with a small taper in October.?

The Fed this week unexpectedly refrained from reducing its $85 billion in monthly asset purchases, saying it needs to see more signs of sustained labor market gains. Chairman Ben S. Bernanke said Sept. 18 the central bank would decide on whether to taper purchases based on ?what?s needed for the economy.?

The Fed will be able to weigh the September jobs report and revisions of prior months as well as updated housing reports at its Oct. 29-30 meeting, Bullard said in a separate interview at Bloomberg?s headquarters in New York. ?This was a very close call so maybe the information would come in in a way that would change the complexion? of the outlook, he said.

Markets shouldn?t have been surprised by the decision because Federal Open Market Committee members have repeatedly said the decision to slow, or taper, would be ?data dependent,? Bullard said.

Slightly ?Dismayed?

?I?m a little dismayed at those in markets that are saying they?re surprised by this,? Bullard said. The Fed said that, ?if the economy was going to improve in the second half of the year, and if we saw that improvement, we would taper.?

Kansas City Fed President Esther George, who has consistently dissented against additional stimulus, said the central bank missed an opportunity to begin reducing bond purchases because markets were primed for such a move.

?Costly steps had been taken to begin to prepare markets for an adjustment in the pace of asset purchases,? George said yesterday in a New York speech. ?This week?s decision by the Fed to taper expectations and not bond buying surprised many, disappointed some like me.?

George has voted this year against all six decisions by the FOMC to press on with bond buying, saying the program risks creating imbalances in the economy and financial markets and pushing up long-term inflation expectations.

Possible Timetable

Bernanke?s remarks earlier this year on the prospect for tapering sent bond yields as much as a percentage point higher. Yields on the benchmark 10-year Treasury note climbed as high as 2.99 percent on Sept. 5 from 1.93 percent on May 21, the day before Bernanke first outlined a possible timetable for a reduction in the asset purchases.

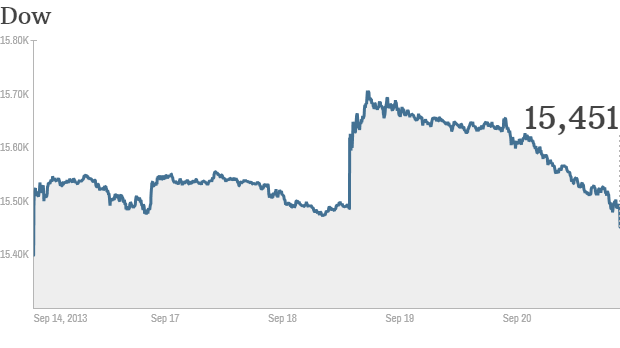

This week?s FOMC decision not to taper helped reverse that rise and pushed back expectations for a tightening of monetary policy. The yield on the benchmark 10-year Treasury note fell yesterday 0.02 percentage point to 2.73 percent in New York, according to Bloomberg Bond Trader prices. The yield earlier rose 0.03 percentage point after Bullard said the FOMC may trim bond buying next month.

Most economists surveyed say the Fed will begin curtailing asset purchases in December. Twenty-four of 41 economists surveyed Sept. 18-19 said the Fed will now wait until December before taking the first step in dialing down monthly bond purchases, according to a Bloomberg survey. The median estimate in an Aug. 9-13 poll projected the Fed would begin paring at this week?s meeting.

Tapering Odds

Investors see a 43 percent chance policy makers will increase the federal funds rate target to 0.5 percent or more by January 2015, based on data compiled by Bloomberg from futures contracts. The odds were 68 percent two weeks ago.

?Rates went up a lot over the summer? and ?for many on the committee that was a surprise,? Bullard said. It wasn?t a ?surprise for me because I?ve said the flow of QE matters a lot.?

So ?when we threatened to pull that back, markets naturally? sent yields higher, he said. Bullard during the past two months has urged the Fed to hold off on adjusting so-called quantitative easing, saying any change should depend on whether inflation moves toward the Fed?s 2 percent target. Policy shouldn?t rely on central bank forecasts for the economy that have proven too optimistic in the past three years, he said.

?We got some weaker data, so that put the committee in a position where we could delay,? he said. With inflation low, Bullard said ?we can afford to be patient.?

Adjust Guidance

The FOMC might also want to adjust its guidance on rates, Bullard said. A ?more likely? scenario than lowering the 6.5 percent unemployment threshold is introducing an inflation floor, Bullard said. The threshold would be something like ?so long as inflation was running below 1.5 percent,? the Fed wouldn?t raise interest rates, he said.

Bullard said he thought 1.5 percent was a good level because it?s ?symmetric? with the 2.5 percent threshold on the ?high side? of the central bank?s 2 percent goal for price increases. Bullard said he doesn?t see the Fed lowering its unemployment threshold.

?I don?t think that?s going to happen,? he said. ?If you move that threshold? it ?loses meaning? as ?markets would rightly think? the Fed could move them around ?for convenience.?

The Fed?s preferred measure of inflation, the personal consumption expenditures index, showed prices rising 1.4 percent in the 12 months ended in July.

?See Evidence?

Bullard, referring to inflation in remarks prepared for a speech in New York, said he wants ?to see evidence? of ?an increase before endorsing less accommodative policy action.?

Bullard dissented from the FOMC?s June 19 policy statement, saying the panel should ?signal more strongly its willingness to defend its inflation goal.? He dropped the dissent at the following meeting when the FOMC added language saying persistently low inflation posed risks to the economic outlook.

Bullard said he disagreed with the committee indicating a plan to taper bonds buying at that point, including stopping purchases in the middle of next year.

?It was premature to lay out the road map? for tapering in June, Bullard said. ?I do think it was a mistake.?

?We should defend our inflation target from the low side,? Bullard said.