x 0 x 0

x 0 x 0

|

Thai will let go if the offer by OUE or other contender is good and compelling enough to reap huge profit. Then we can benefit from a huge dividend I hope.

bikerlover ( Date: 22-Oct-2012 11:58) Posted:

They will not let it go.

shadowmoon ( Date: 20-Oct-2012 18:12) Posted:

Got this feel, the Thai will let go bro.

Let see how things move.

Rem the Thai Boss say b4 he will not spend too much to take over F& N.

N if he is interested, in beverage business. Singapore got some more better company to target.

Strong feeling as others, the Thai will cash out .....hehe..

Hope so. If that the case, THaiBev will cheong.

Cheerio |

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Hope it sells to OUE for a huge profit and give out generous dividends!

skk888 ( Date: 19-Oct-2012 17:11) Posted:

Take a punch of salt with terms like "may", and "one of the companies". It can mean "may not" and "one of the other companies", they have equal probabilities.

But it's kirin, it'll be very challenging for thaibev if they want to continue with the bid. Better option is to exit. Thaibev gearing is high and currently rated BBB..

bluechip138 ( Date: 19-Oct-2012 17:04) Posted:

(Reuters) - A Singapore hotel and property firm backed by Indonesia's Lippo Group may team up with Japan's Kirin Holdings to thwart a $7.2 billion takeover offer for Fraser and Neave Ltd (FRNM.SI) from companies linked to Thailand's third-richest man, sources said.

In an unexpected move, Overseas Union Enterprise Ltd (OUE) (OVES.SI) said on Friday it is seeking partners in a potential takeover bid for F& N, without identifying the parties. Kirin Holdings Co Ltd (2503.T) is one of the companies involved in the preliminary discussions, said the sources, who spoke on condition of anonymity because the talks were private.

====

So it is Kirin, exciting bidding war ahead?

|

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

All food stocks are overated because of F& N. Yeo Hiap Seng is falling and will continue to fall to realistic value.

dicksonh ( Date: 18-Oct-2012 10:27) Posted:

| With all the stocks moving up, this should be doing better than now? |

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Good time to take profit. The low this morning was 74 cents. Now it is above 90 cents

Juzztrade ( Date: 18-Oct-2012 13:22) Posted:

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Better to trade the odd lots during the window period. After the last day, though can still trade, it may not be easy to find buyer/seller as the volume will be low

iodium ( Date: 17-Oct-2012 11:45) Posted:

Hi tonylim, thanks for the info.

But from the following schedule, am I correct to say that 1 can keep my 500 triyard shares and trade it within 18 Oct to 16 Nov to sell them or buy 500 triyard? Buying or selling my EZRA is out of question for my current condition. And what will happen if I still hold on 500 triyards after 16 November?

Expected date for the commencement of trading of odd-lots of Triyards Shares on the SGX-ST: Thursday, 18 October 2012 at 9.00 a.m.

Expected last date of trading of odd-lots of Triyards Shares on the SGX-ST: Friday, 16 November 2012

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

You will get 500 Triyard shares which is worth about .80 per share (need to confirm). You can sell them as odd lot. The other way is to buy 5 lots of EZRA to make up to 10 lots and get 1 lot of Triyard. Or sell your 5 lots of EZRA.

iodium ( Date: 16-Oct-2012 16:38) Posted:

I have 5 lot of ezra. I think it makes me entitle with 500 triyards shares.

What will happen if I keep my 500 shares (oddlots right?) pass 16 November?

JYJY93 ( Date: 09-Oct-2012 17:06) Posted:

Because from what i seen their announcement:

Expected Books Closure Date for the Distribution : Thursday, 11 October 2012 at 5.00 p.m.

Expected date for the crediting the Triyards Shares into the Securities Accounts of Entitled Depositors: Wednesday, 17 October 2012

Expected date for the commencement of trading of Triyards Shares on the SGX-ST : Thursday, 18 October 2012 at 9.00 a.m.

Expected date for the commencement of trading of odd-lots of Triyards Shares on the SGX-ST: Thursday, 18 October 2012 at 9.00 a.m.

Expected last date of trading of odd-lots of Triyards Shares on the SGX-ST: Friday, 16 November 2012

I thought i need to hold until 11 October. So now i get why this stock drops, its because everyone got the dividends already... |

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Anthony Tan, it is coming...be patient

tonylim ( Date: 16-Oct-2012 13:59) Posted:

It is not in the sleep mode but rather accumulation phase at .565 and 57. Understand once all borrowings are cleared, this is the stock to watch.

AnthonyTan ( Date: 30-Mar-2012 15:00) Posted:

| Still sleeping, no movement at all. |

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

It is not in the sleep mode but rather accumulation phase at .565 and 57. Understand once all borrowings are cleared, this is the stock to watch.

AnthonyTan ( Date: 30-Mar-2012 15:00) Posted:

| Still sleeping, no movement at all. |

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Trying to raise the take-over price. Good luck if you buy now.

newbie86 ( Date: 15-Oct-2012 22:08) Posted:

| Any reason why it is not stopping? |

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Midas will show its color when you least expect it. Trust your own judgement and never waver and switch gear based on negative remark. All things look positive for Midas. It just a matter of time it will shine. So just dream and let it come true.

Bopanha ( Date: 16-Oct-2012 13:18) Posted:

It is good to have a dream. All things are made possible through the dreams of man. It is not impossible for Midas to retrace its path to its highest. Lol.

Must we be reminded that Ristakers always talk opposite? Ask Junwei, he will ans +vely. Lollol.

risktaker ( Date: 16-Oct-2012 12:27) Posted:

| U haven't wake up is it..... lol .... |

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

PEC is starting to move upwards. Good showing this afternnon with good volumn

tonylim ( Date: 01-Oct-2012 13:59) Posted:

I would think otherwise and should be moving upwards :

By Chia Jiunyang

Mon, 17 Sep 2012, 09:13:32 SGT

PEC Ltds (PEC) share price has fallen by almost half from its peak of S$1.37 per share in Jan 2011 and may have already bottomed out. We now see very deep value in the group, with its stock trading at 13% discount to its book value of S$0.79 per share with a net cash of S$0.44 per share or 64% of its market capitalization. Excluding its net cash value, it is trading at just 3x PER. Meanwhile, our channel checks inform us that the current pricing levels are too tight for the downstream EPC subcontractors to bear, and are unsustainable in the long run. We agree and therefore believe that a margin reversion may be possible in the near- to medium- term horizon. Upgrade to BUY with a higher fair value estimate of S$0.86 (previously S$0.64).

Deep value

PEC Ltds (PEC) share price has fallen by almost half from its peak of S$1.37 per share in Jan 2011 and may have already bottomed out. Year-to-date, its share price has also been uninspiring, hovering mostly around the S$0.60-S$0.70 region. We now see very deep value in the group, with its stock trading at 13% discount to its book value of S$0.79 per share with a net cash of S$0.44 per share, or 64% of its market capitalization. Excluding its net cash value, it is trading at just 3x PER.

Rotterdam issues over

Previously, investors were concerned about PECs cost over-run issues at its Rotterdam JV project. With its S$17.3m allowance for its debt against the JV company Verwater-Audex B.V. in 4Q12, PEC has finally reached a closure on the issue. We do not expect further write-offs. Looking ahead, we believe the management will focus its energies on growing its business in the Middle East and Southeast Asia regions.

Upgrade to BUY FV raised to S$0.86

We see deep value for PEC and believe that margin reversion is possible. Therefore, we raised our fair value estimate to S$0.86 (previously S$0.64) on 1x (previously 0.8x) P/B. Upgrade to BUY.

|

|

|

|

Sgshares ( Date: 01-Oct-2012 13:50) Posted:

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

They actually meant it is undervalued at its current price. Anyway, just bought some just in case.

phil1314 ( Date: 04-Oct-2012 22:38) Posted:

I am always weary when analyst highlight shares trading below its fair value when there is no liquidity in the counter. Roxy Pacific, GuocoLeisures plus many others are all in the same category and prices hardly move above the fair value for many years

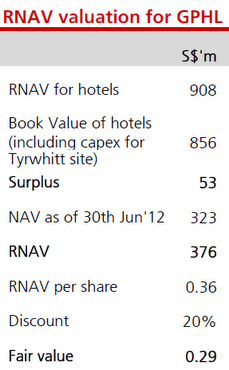

sanuks ( Date: 17-Sep-2012 09:35) Posted:

DBS Vickers, first to cover GLOBAL PREMIUM HOTELS, says its fair value is 29 cents

Source: DBS Vickers

Analyst: Derek TAN CPA

Household name in the Economy hotel space

Resilient operating model with portfolio expansion from the development of a new 265-room hotel

Fair value of S$0.29 based on 20% discount to RNAV

Fair

value of S$0.29. Given GPHLs leading position in the economy tier

segment of the Singapore hotel sector, we derive a fair value of S$0.29,

based on a 20% discount to its RNAV of S$0.36.

This implies FY14F EV/EBITDA of 17x, in line with hospitality peers.

Earnings

upgrade will be a price catalyst. Better than expected performance from

its hotel segment in the coming quarters or acquisitions not factored

in our forecasts are likely to drive profitability and stock price.

Balance

sheet is relatively highly geared. GPHLs net debt to equity ratio is

relatively high at 1.4x, due to acquisition of its initial portfolio

upon listing.

We noted that other metrics, such as interest cover, is comfortable at c.4-5x.

|

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Today Midas looks set to surge

yabbest ( Date: 04-Oct-2012 19:58) Posted:

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

UOB Kay Hian says Sell with a TP of $2.40 but price shot up on the same day ! Such ridiculous analysis by Kay Hian ! Can trust what they say?

Kensonic77 ( Date: 04-Oct-2012 21:06) Posted:

Stock always give surprise

Luckily didn't listen to them

KEY HIGHLIGHTS from a Brokerage

SATS (SATS SP/SELL/S$2.77/Target: S$2.40) Page 2

Flight cancellations on China-Japan routes a cause for concern |

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Riding on Singapore Brand Name.

All it needs now is announcement of new projecs before breaking the 43 cents barrier

gavinl ( Date: 04-Oct-2012 06:09) Posted:

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Earlier there was buy up because of the share dividend to make it up to 10 lot to get 1 lot of Tyraid

Now it seems there are those letting go of the loose lots (< 10 lots) to avoid getting odd lots

cheekong22 ( Date: 03-Oct-2012 11:22) Posted:

|

sell down as usual with considerable high volume.

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

What would happen to F & N share price if the takeover is not successful? How much would it fall?

bluechip138 ( Date: 02-Oct-2012 10:22) Posted:

F & N has gone back up to $8.92 while TB is stagnant at $0.395. It will be tough takeover battle ahead for TB.....

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

I would think otherwise and should be moving upwards :

By Chia Jiunyang

Mon, 17 Sep 2012, 09:13:32 SGT

PEC Ltds (PEC) share price has fallen by almost half from its peak of S$1.37 per share in Jan 2011 and may have already bottomed out. We now see very deep value in the group, with its stock trading at 13% discount to its book value of S$0.79 per share with a net cash of S$0.44 per share or 64% of its market capitalization. Excluding its net cash value, it is trading at just 3x PER. Meanwhile, our channel checks inform us that the current pricing levels are too tight for the downstream EPC subcontractors to bear, and are unsustainable in the long run. We agree and therefore believe that a margin reversion may be possible in the near- to medium- term horizon. Upgrade to BUY with a higher fair value estimate of S$0.86 (previously S$0.64).

Deep value

PEC Ltds (PEC) share price has fallen by almost half from its peak of S$1.37 per share in Jan 2011 and may have already bottomed out. Year-to-date, its share price has also been uninspiring, hovering mostly around the S$0.60-S$0.70 region. We now see very deep value in the group, with its stock trading at 13% discount to its book value of S$0.79 per share with a net cash of S$0.44 per share, or 64% of its market capitalization. Excluding its net cash value, it is trading at just 3x PER.

Rotterdam issues over

Previously, investors were concerned about PECs cost over-run issues at its Rotterdam JV project. With its S$17.3m allowance for its debt against the JV company Verwater-Audex B.V. in 4Q12, PEC has finally reached a closure on the issue. We do not expect further write-offs. Looking ahead, we believe the management will focus its energies on growing its business in the Middle East and Southeast Asia regions.

Upgrade to BUY FV raised to S$0.86

We see deep value for PEC and believe that margin reversion is possible. Therefore, we raised our fair value estimate to S$0.86 (previously S$0.64) on 1x (previously 0.8x) P/B. Upgrade to BUY.

|

|

|

|

Sgshares ( Date: 01-Oct-2012 13:50) Posted:

down

ballball ( Date: 01-Oct-2012 13:45) Posted:

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Other than poor palm oil price (already factored in current price), there is no reason for it to move downwards any further unless the world economy worsen and stock market takes a tumble.

New123 ( Date: 01-Oct-2012 12:23) Posted:

What is yr view? Is it cont going up stream this wk?

rutheone1905 ( Date: 27-Sep-2012 13:51) Posted:

this week is qtr end GAR being STI components stock maybe support due to window dressing.

next week institutes may start dumping....so fifo better |

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Pretty good dividend payable on 26 Nov, you get $250 for 10 lots :

| PEC |

SGD0.025 |

Nov 8 (ex cd) |

Nov 26 |

stu4rt86 ( Date: 01-Oct-2012 12:31) Posted:

| PEC on CD? what it means sia

|

|

|

|

Good Post

Bad Post

|